ECOLOGICAL ACCOUNTING – WHAT’S IN A NUMBER? “Start with an understanding of the parcel because that is how communities regulate and plan land use. It is the parcel level where you get the information that you need to change practice to protect natural assets. That is what everyone must get their heads around,” stated Tim Pringle (October 2022)

Note to Reader:

Waterbucket eNews celebrates the leadership of individuals and organizations who are guided by the Living Water Smart in British Columbia: The Series vision. The edition published on October 18, 2022 featured the story behind the story of the pattern of discovery by Tim Pringle that resulted in development of the methodology and metrics for EAP, the Ecological Accounting Process.

“We needed a measure of financial value that could be applied on stream systems generally, not just because somebody somewhere had done something somehow. And then it struck me, the BC Assessment database is the lynchpin for financial valuation.” – Tim Pringle

How will communities ensure that streams survive as healthy ecosystems in an urban setting? This existential question defines a key challenge facing local governments in an era of weather extremes. EAP, the Ecological Accounting Process, provides communities with a path forward. It is the means to inject balance into the natural asset management conversation.

The urgency of the drainage liability issue spurred EAP development. The Drainage Service is the neglected municipal service, and the cost of neglect grows over time. The consequence of neglect is an accumulating financial liability to fund creek channel stabilization and riparian corridor restoration in urban and urbanizing settings.

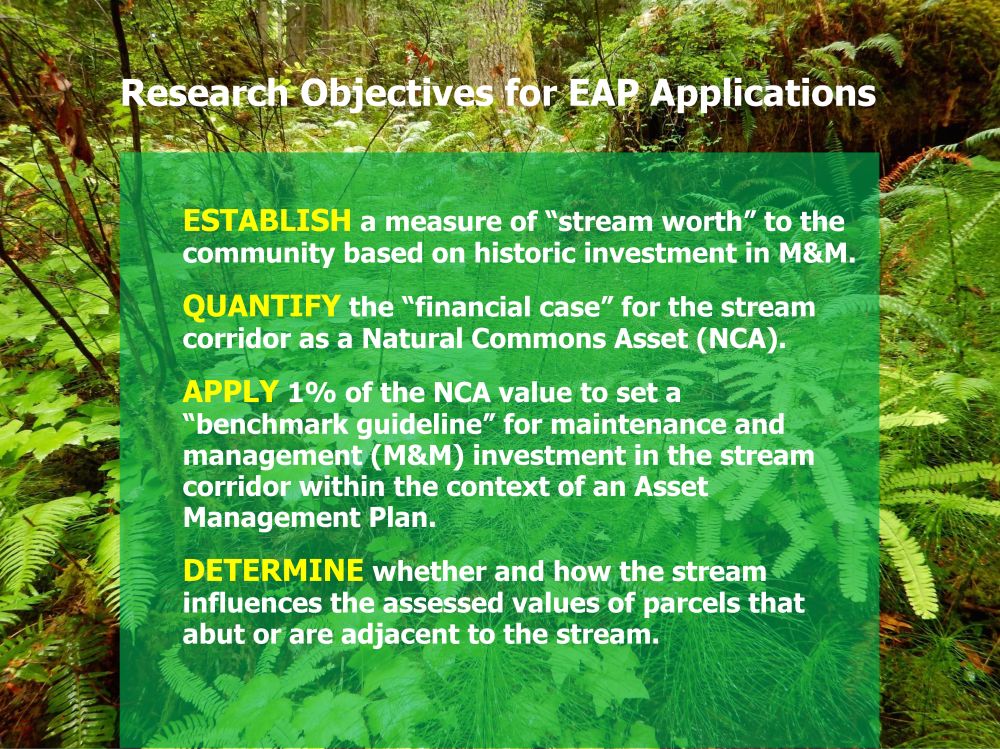

The EAP methodology and metrics enable communities to make the financial case for maintenance and management (M&M) of stream systems. Local governments need real numbers to deliver green infrastructure outcomes. It is that basic. Rhetoric is insufficient. EAP metrics are grounded in the BC Assessment database.

The strength, uniqueness and power of EAP is that the methodology yields a defensible number. In turn, this provides a sound basis for an annual M&M budget and all the decisions that flow from having that capability. The methodology is universal, but application is guided by the issues specific to each creek situation. It is the exact opposite of a cookie-cutter approach.

Cascading Concepts: Five Key Ideas that Underpin EAP

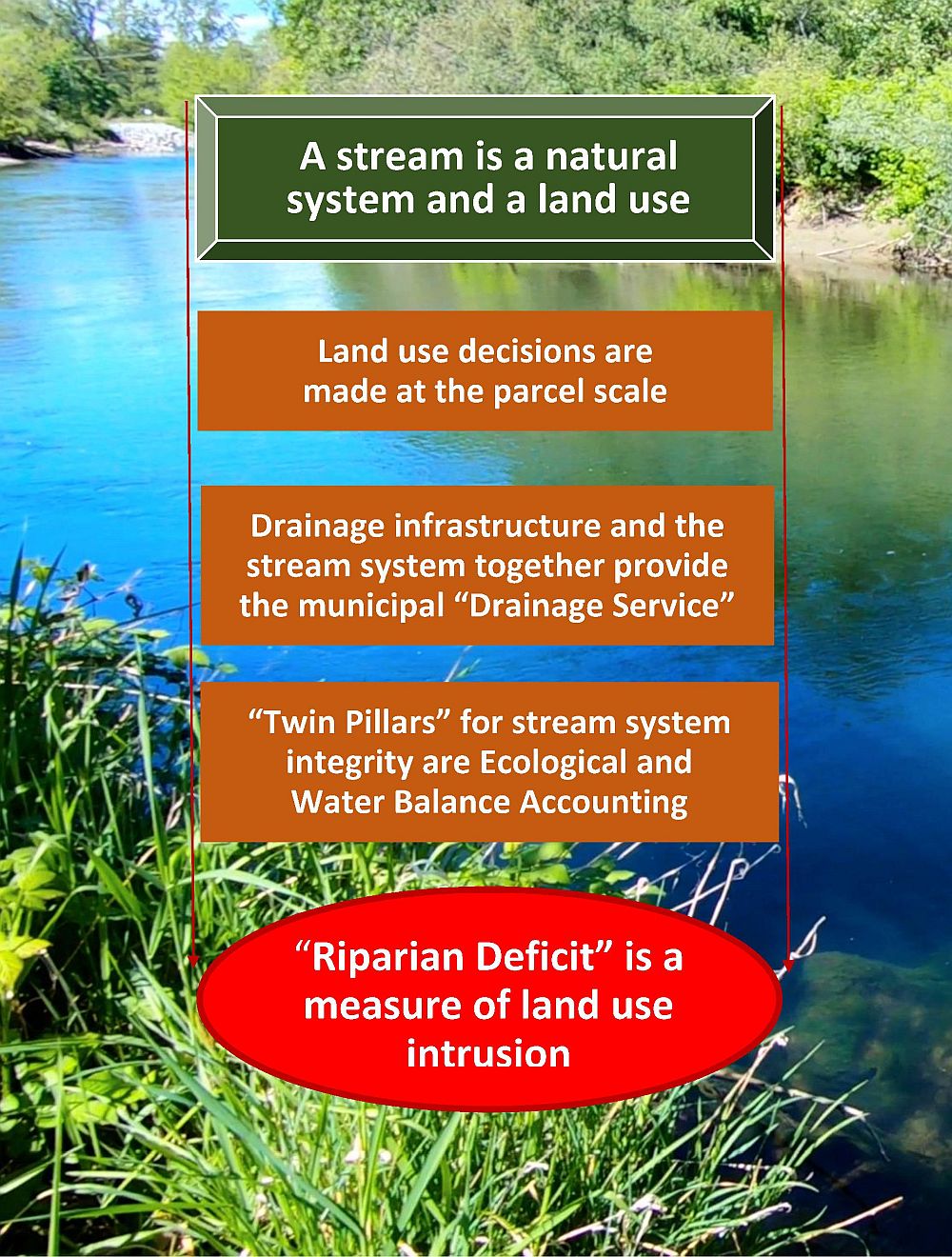

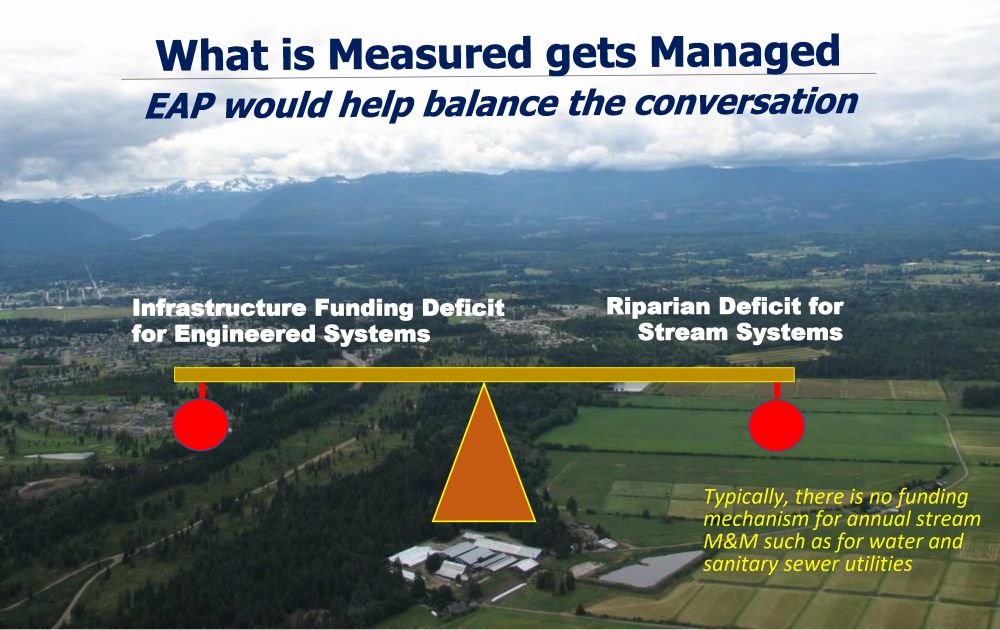

The Riparian Deficit is the environmental equivalent of the Infrastructure Funding Deficit (or Gap). It puts the environmental perspective on an equal footing with the engineering and accounting perspectives. This is game-changing.

Because stream setbacks are defined in regulation, a stream corridor is a land use such that a proxy financial value is readily determined from BC Assessment data.

TO LEARN MORE, DOWNLOAD: Ecological Accounting Process, A B.C. Strategy for Community Investment in Stream Systems (2022)

EDITOR’S PERSPECTIVE / CONTEXT FOR BUSY READER

“In this edition, the Partnership for Water Sustainability’s Tim Pringle shares the story behind the story of the ‘pattern of discovery’ that led him to the BC Assessment database. In developing the EAP methodology and metrics, he has demonstrated that ‘the parcel’ is the lynchpin for integrating line items for M&M of streams systems in asset management budgets,” stated Kim Stephens, Waterbucket eNews Editor and Partnership Executive Director.

“Local government elected representatives and staff understand the parcel perspective because this is what they work with every day,” Tim Pringle reminds us. “Getting it right about financial valuation of ecological services starts at the parcel scale and recognizing that every parcel is interconnected within a system.”

“Three decades ago, the philosophy that ‘use and conservation of land are equal values’ launched Tim Pringle on a career trajectory that has culminated with his breakthrough accomplishment in leading the EAP initiative. EAP opens ups multiple pathways for local governments to achieve the goal of ‘natural asset management’.”

“Now, with EAP as a foundation piece, maintenance and management (M&M) of stream systems can be integrated into a Local Government Finance Strategy for sustainable infrastructure funding to tackle the Riparian Deficit.”

STORY BEHIND THE STORY: Ecological Accounting – What’s in a NUMBER?

The EAP methodology and metrics evolved over the course of a 6-year program of applied research. The program involved 9 demonstration applications (case studies) and 13 local governments on Vancouver Island and in the Lower Mainland regions of the Georgia Basin.

The first two stages were TEST and REFINE the methodology, respectively. Each stage comprised two projects. Stage 3 then involved 5 more projects to demonstrate how to operationalize EAP within local government processes.

“Stage 3 is the springboard to embedding EAP in the Mount Arrowsmith Biosphere Research Institute at Vancouver Island University. This will ensure knowledge of EAP is maintained and passed on to the next generations of planners and local government staff,” states Tim Pringle.

The Pattern of Discovery

“We began by looking at research elsewhere in Canada and internationally that is concerned with ecological values. We quickly realized that we had to distinguish between ecological services and the natural assets themselves.”

“To look at the financial value of natural assets in a meaningful and universally applicable way, the key is how you identify the physical asset which delivers the ecological services.”

What is a useful measure?

“The first two building blocks were Busy Place Creek and Brooklyn Creek in the Cowichan and Comox valleys, respectively. Collaboration with two wiling local governments allowed us to test our ideas by exploring possibilities.”

“With Busy Place Creek, we initially looked at whether and how a universal average expenditure per unit area might be used for valuing potential wetland restoration along streams. In the end, we concluded that the available information is not useful because it is project-specific. In short, no methodology emerged from the numbers.”

What became clear

“The breakthrough came when we turned our attention to Brooklyn Creek. The Town of Comox had spent $2 million in 2005 to construct a peak flow diversion pipe. It then embarked on a multi-year program to stabilize, maintain and enhance the creek corridor and streamside riparian areas.”

“But, I wondered, what is the Brooklyn Creek experience telling us that we could apply to other streams? How do we get useful and replicable numbers for financial valuation of ecological services? This question led me to look for a way to think about what we could meaningfully measure, other than using cash outlays for site-specific projects.”

BC Assessment is the Lynchpin

“I soon realized that we needed to make a distinction between WORTH and VALUE. Worth reflects community willingness to invest in the stream. That led to the next leap – to go from looking at things related to worth, and consider things related to the value of the actual physical area of the stream corridor system.”

“We needed a measure of financial value that could be applied on stream systems generally, not just because somebody somewhere had done something somehow. And then it struck me, the BC Assessment database is the lynchpin for financial valuation.””We immediately realized that improvements on a property are not relevant. Thus, we only use the land portion of the BC Assessment database. We make a clear distinction between parcel values and property values.”

What is Measured gets Managed

“The EAP methodology considers a stream corridor and its protected setback zone to be a land use because it is defined in regulation. EAP defines the regulated zone as the Natural Commons Asset. And it has a financial value which we determine through an analysis of parcel data using BC Assessment for sample groups of parcels abutting and adjacent to streams.”

“With Brooklyn Creek, we now had a defensible dollar number, expressed as a unit value, which we could apply over a stream length. In Stages 2 and 3, we validated the usefulness of EAP through application of a consistent set of research questions and objectives to seven subsequent case studies.”

“From start to finish, it was a building blocks process. Understanding what each local government partner needed as an outcome from their EAP project became a critical consideration. EAP evolved as one ‘big idea’ led to the next one. We could not have made the leap directly from the first to the last. It required a building blocks process.”

Reduce the Riparian Deficit

“Although the research framework is common to all, each EAP case study is unique. Each local government is dealing with a distinctive stream system management challenge driven by local circumstances.”

“Think of EAP as a basic methodology plus add-ons. The latter are the questions that local governments have about where and how EAP fits into a strategic question. It is those questions that are shaping the evolution of EAP.”

|

|

DOWNLOAD A COPY OF https://waterbucket.ca/gi/wp-content/uploads/sites/4/2022/06/EAP-Synthesis-Report-Beyond-the-Guidebook-2022_Jun-2022.pdf